What Is a Bill of Entry (BOE)? Complete Guide with BOE Status Meaning, IGST Process & Mistakes

Complete Bill of Entry guide: Types, format, BOE filing process, status tracking on ICEGATE, GST integration, common mistakes & compliance checklist for importers

Listen to article

Audio version (0% complete)

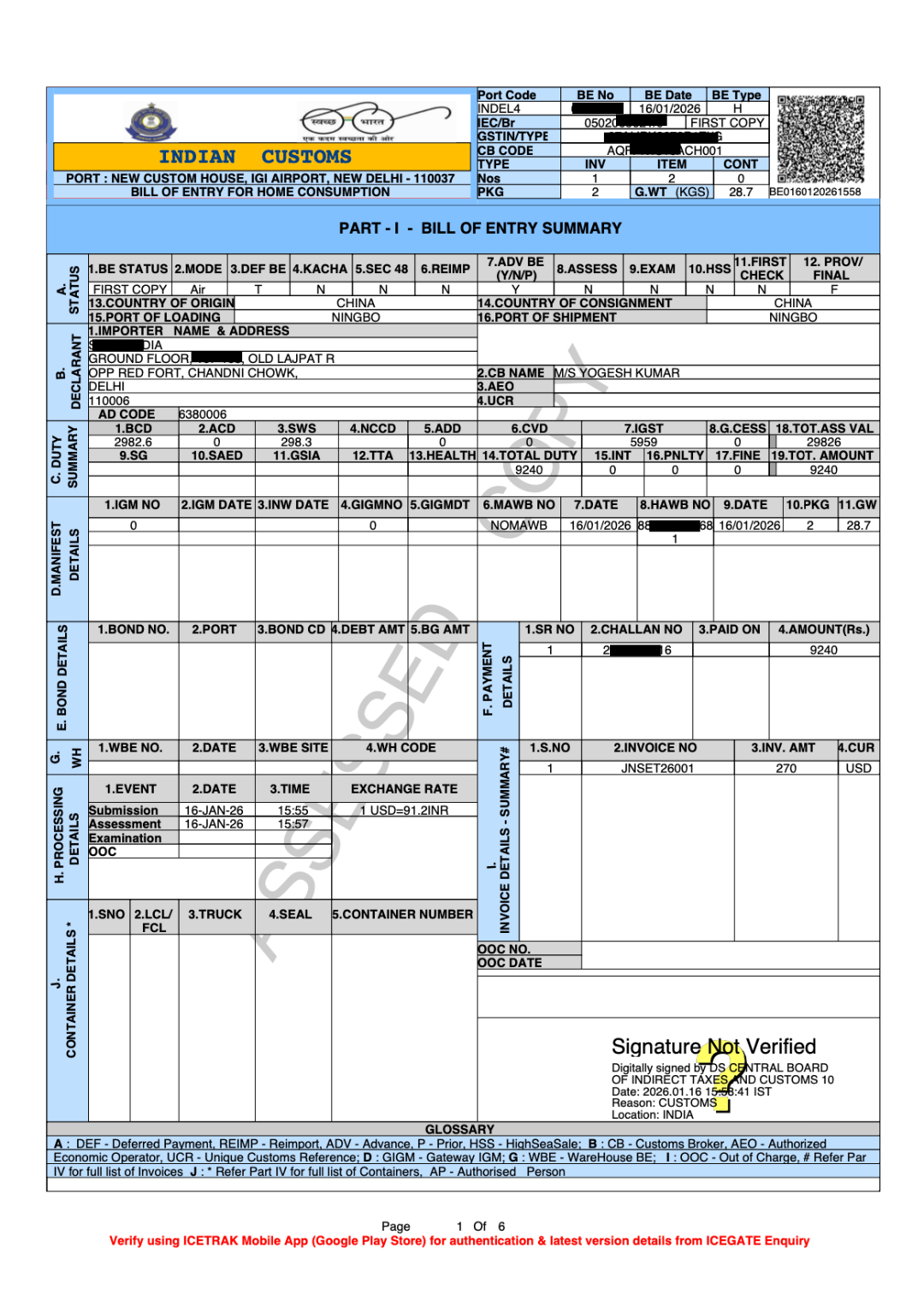

A Bill of Entry (BOE) is the mandatory legal declaration an importer or their Customs House Agent (CHA) files with the Indian customs department when goods arrive at a sea port, airport or ICD. Before BOE filing, the shipping line/ Airline records the cargo through the Sea/ Air IGM (Import General Manifest) which you can track on ICEGATE to confirm your consignment has been manifested on arrival or not, without IGM shipment cannot be cleared from customs. BOE is the primary document in the customs clearance process, containing details such as the importer’s IEC and GSTIN, CHA code, description of goods, HS code, quantity, value, and applicable customs duties and taxes.

Customs officers use the BOE to verify that your goods comply with Indian customs regulations, determine the applicable duties and goods and services tax (IGST), and decide whether the shipment can be released into India. Without a correctly filed BOE, customs cannot complete proper customs processing, no duties or IGST can be assessed, and your cargo cannot obtain customs clearance, leading to delays and storage charges.

What Is a Bill of Entry (BOE)?

A Bill of Entry (BOE) is fundamentally a customs clearance declaration. The main purpose of BOE is the assessment of customs duty. When imported goods arrive at an Indian Sea port, Airport, or Inland port, the importer or their authorized Customs House Agent (CHA) must file a BOE with customs authorities for the timely clearance of goods.

BOE vs. Bill of Lading (B/L): Understanding the Difference

Many importers confuse Bill of Entry (BOE) with Bill of Lading (B/L). These are completely different documents. Below are some of the major differences:

Aspect | BOE | B/L |

|---|---|---|

When Issued | AFTER goods arrive at port | BEFORE goods leave exporter |

Who Issues | Customs issues | Shipping company issues |

Required For | Customs Clearance | Shipping container formalities |

Legal Requirement | Mandatory under Customs Act 1962 | Mandatory for international freight |

Format | Digital (ICEGATE filing) | Physical + Digital copies |

Transferable | NO (specific to one importer) | YES (can be endorsed/transferred) |

Types of Bill of Entry: Which One Do You Need?

Different forms of BOE exist depending on what you plan to do with the goods, and choosing the wrong type can delay smooth customs clearance. The three main types used in India are:

Type 1: BOE for Home Consumption (Most Common)

This is the most common form, filed when imported goods are meant for immediate domestic use, sale, or manufacturing after payment of all applicable duties and taxes. The BOE for home consumption is used when you want cargo released directly into the Domestic Tariff Area (DTA) after customs clearance procedure is complete and Out of Charge is granted.

The customs officer assesses basic customs duty, IGST (part of the goods and services tax system), and any other cesses or charges, once paid in full and examination (if any) is satisfactory, the goods are cleared for home consumption.

Type 2: BOE for Warehousing (Bonded Warehouse)

A Bill of Entry for warehousing (also called an Into‑Bond BOE) is filed when the importer wants to move goods from the port into a customs‑bonded warehouse without immediately paying customs duty and IGST. This helps manage cash flow, because duties are deferred until the goods are actually needed and cleared from the warehouse, while customs maintains control over the cargo.

This BOE is common for importers with fluctuating demand or longer sales cycles, who want stock closer to market but prefer to delay cash outflow on duties.

Type 3: BOE for Ex-Bond Clearance

An Ex‑Bond Bill of Entry is filed when goods previously warehoused under Into‑Bond BOE are finally released for home consumption and the applicable duties and IGST are paid at that stage. In this case, duty rate and exchange rate are applied as on the date of ex‑bond clearance, not the original date of import, which can be favourable or unfavourable depending on rate movements.

Type 4: BOE for Re-Export

Beyond these three, there are special BOE types for re‑imports, transshipment and project imports, and specific procedures for Special Economic Zones (SEZs). SEZ units, for example, file BOEs with customs officers posted in the zone using specially endorsed forms (“SEZ Cargo”) and follow distinct rules when moving goods between SEZ and DTA.

The Bill of Entry Format

While most BOEs are now filed electronically via ICEGATE, the underlying format is standard and understanding it helps ensure proper customs processing. A typical BOE format for home consumption includes:

- Importer details: name, address, IEC, GSTIN, and contact information.

- CHA details: name and Customs House Agent code, if a customs broker is filing on your behalf.

- Shipment and port details: port code, vessel or flight details, Bill of Lading/AWB number, country of origin and shipment.

- Goods details: description, HS code, quantity, unit price, currency, and assessable value.

- Duty and tax details: applicable customs duties, IGST and other charges, along with exemption notification references if any apply.

The BOE also becomes the official record of the import transaction used in the importer’s accounts, for internal controls and for future customs and GST audits. Maintaining BOE copies and linking them properly to purchase entries and IGST payments is critical for both compliance and smooth reconciliations.

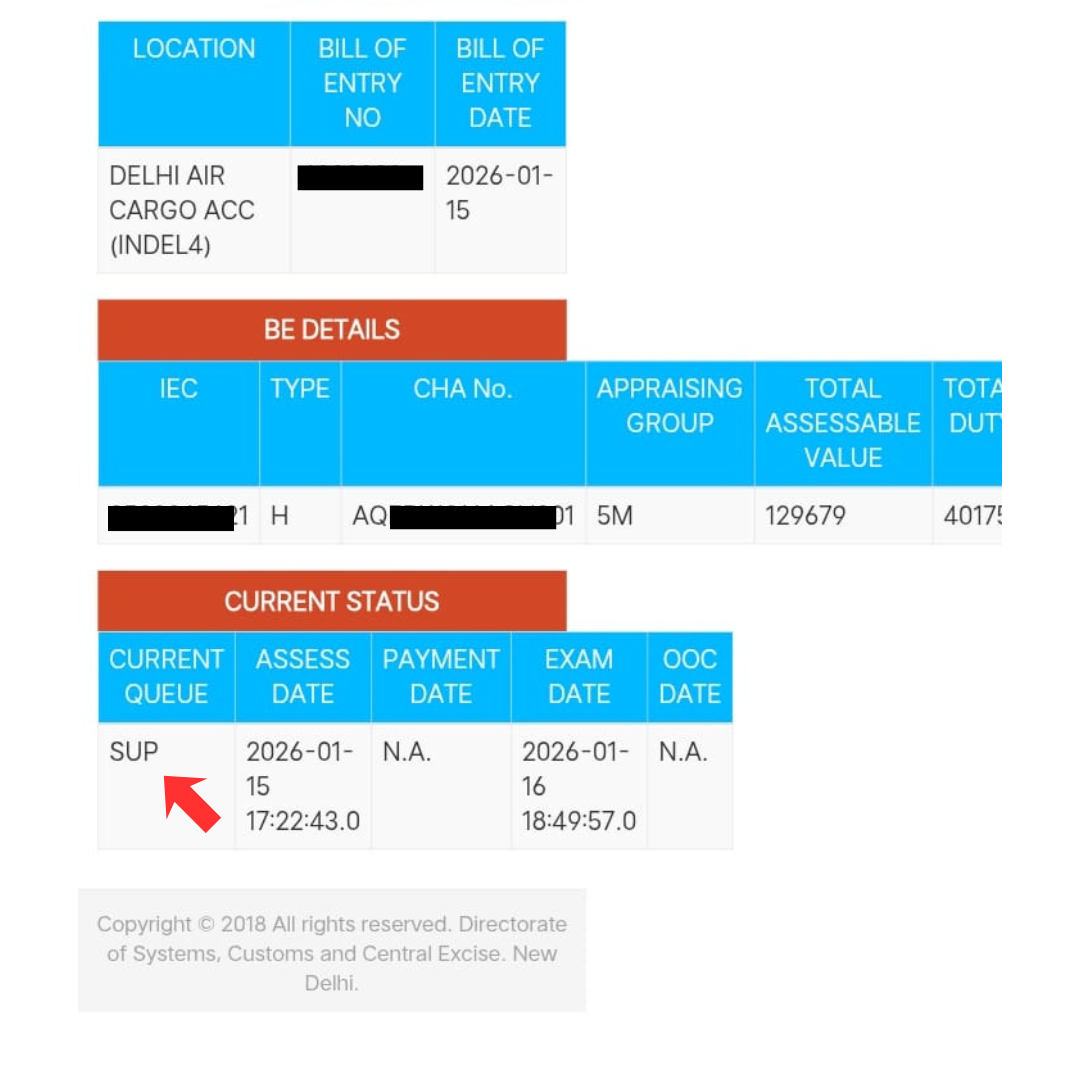

Bill of Entry Status: Understanding BOE Status on Icegate

Your shipment's BOE goes through several statuses as customs processes it. Tracking Bill of Entry status on ICEGATE is crucial because it tells you exactly where your shipment stands and when you can collect it.

The Four Main BOE Status Types

Status 1: "Under Assessment"

Customs is currently reviewing your BOE, checking document accuracy, and verifying HS codes and duty calculations.

Status 2: "Assessment Complete" (or "Duty Assessed")

Customs has verified all details and calculated the exact duties and taxes you must pay. Pay duties immediately through Icegate portal channels. Delay in payment attracts interest on duty and demurrage charges.

Status 3: "Out of Charge" (Clearance Complete)

CUSTOMS HAS FULLY CLEARED YOUR SHIPMENT. All documents are verified, duty and taxes are paid, goods have been examined (if required) and now ready for collection.

Status 4: "Query Raised" or "Pending Clarification"

Customs has questions or concerns about your shipment and needs additional information before clearing it. For example:

- HS code discrepancy

- Value mismatch

- Missing or incomplete documents

- Restricted item classification confusion

Filing Deadline and Late Filing Rules

Under the amended Section 46 of the Customs Act, importers must now file the Bill of Entry by the end of the day (including holidays) preceding the day of arrival of the vessel, aircraft or vehicle carrying the goods. This advance filing facilitates pre‑arrival assessment and significantly reduces clearance time if everything is in order.

If the BOE is filed late, customs can impose late filing fees and other penalties, and late filing often means longer dwell time, higher demurrage, and a disrupted customs clearance procedure. Treat the BOE filing deadline as a hard cut‑off in your import planning.

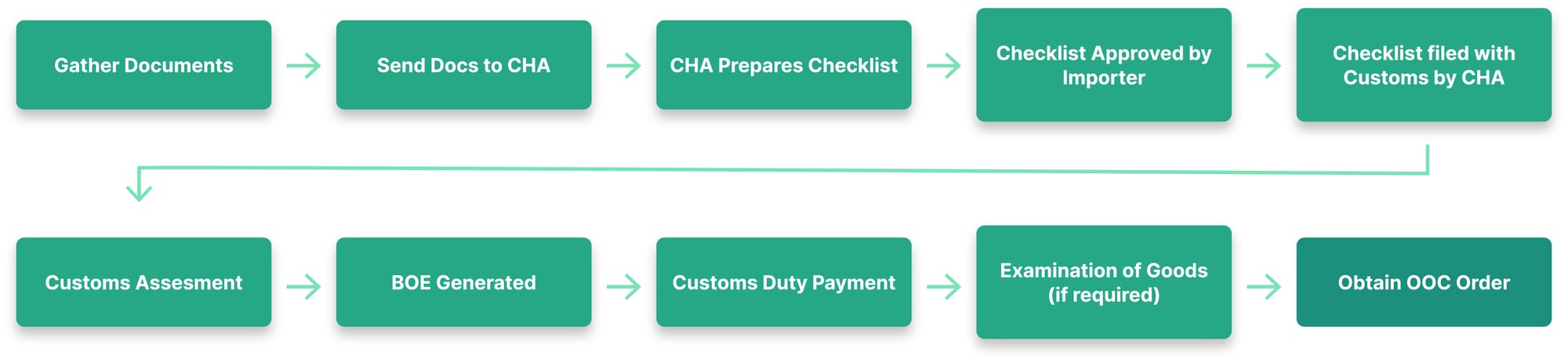

Bill of Entry Filing Process: Step‑by‑Step

In practice, most importers work with a CHA, but as an importer you should still understand the high‑level steps in the BOE filing process.

1. Prerequisites and Registrations

Before filing any BOE you must:

- Obtain a valid Import Export Code (IEC) from DGFT.

- Register your IEC and GSTIN on the ICEGATE portal and set up user credentials.

- Procure and register a Class 3 digital signature certificate (DSC) for secure submissions.

Without these, neither you nor your customs broker can file BOEs electronically.

2. Document Preparation

To file a BOE, the importer or their customs agent must submit key documents to customs, typically through ICEGATE and the e‑Sanchit document upload system. Common documents include:

- Commercial invoice and packing list.

- Bill of Lading or Airway Bill.

- Import licence or authorisations (if required for restricted goods).

- Insurance certificate and freight details.

- Certificate of origin, test certificates, and other regulatory approvals where applicable.

- IEC and GST registration proof, along with CHA authorisation if a broker is used.

Preparing these correctly upfront is essential for smooth customs clearance.

3. Electronic BOE Filing on ICEGATE

The importer or CHA logs into ICEGATE, selects the appropriate port and BOE type (home consumption, warehousing, ex‑bond), and fills in all required shipment and goods details. Data can be submitted via webform, RES package, or authorised third‑party applications, and supporting documents are uploaded electronically.

Once submitted, ICEGATE generates a BOE number and acknowledgement, which is used for all further communication and tracking.

4. Customs Assessment, Queries and Examination

Customs officers review the BOE to ensure that HS classification, valuation, exemption claims, and declared origin are accurate and in line with customs regulations. The system may assign the BOE for documentary checks only or for physical examination depending on risk parameters.

If any mismatch is found—such as invoice value not matching the BOE, or HS code inconsistent with the product—customs raises a query that must be replied to promptly through ICEGATE to avoid delays.

5. Duty Payment and Final Clearance

After assessment, ICEGATE computes applicable customs duties, IGST and other charges, and the importer pays electronically through authorised banking channels. On confirmation of payment and satisfactory completion of checks, the BOE status changes to Out of Charge, allowing your CHA or transporter to move the goods from the port/ICD to your warehouse or factory.

This overall flow - document submission, customs assessment, duty payment, and release of goods, is the backbone of the customs clearance procedure for imports in India.

Common BOE Mistakes That Cause Delays & How to Avoid Them

Common BOE Mistakes That Cause Delays

Many clearance delays are self‑inflicted and come from inaccurate or incomplete BOE filings rather than “slow customs”. Key mistakes to avoid:

- Incorrect HS code classification - Misclassifying goods (for example, declaring smartphones under a feature‑phone code) leads to wrong duty, queries, and sometimes re‑assessment and penalties.

- Undervaluation - Declaring a lower value than the commercial invoice in an attempt to reduce duty exposes the importer to reassessment, fines, and tighter scrutiny.

- Wrong importer or GSTIN details - Missing or incorrect IEC, GSTIN or address details prevent customs and GST systems from matching records and can block IGST credit later.

- Missing licences or approvals - Filing a BOE without mandatory import licences, product registrations or NOCs for restricted or regulated items guarantees queries and delays.

- Inconsistent documentation - Differences between invoice, packing list and BOE (quantities, values, or descriptions) are a common trigger for queries and examinations.

In short, failure to file a BOE correctly, especially with mismatched invoice values or HS codes versus supporting documents can seriously delay clearance and increase costs.

BOE and GST Integration: Claiming Input Tax Credit (ITC)

One major reason BOE matters for GST purposes is that it's your gateway to claiming input tax credit (ITC) on imported goods.

How BOE Links to GST ITC

When you import goods:

- You pay IGST at customs (on imported goods)

- BOE is filed with your GSTIN

- ICEGATE shares BOE data with GST system

- GST system automatically populates GSTR-2A (purchase return)

- You claim ITC on IGST paid

- Reduces your GST liability

Example:

Shipment Value: ₹10 lakh

Basic Customs Duty (15%): ₹1.5 lakh

IGST (18% on ₹11.5L): ₹2.07 lakh

Total Tax Paid: ₹3.57 lakh

GST ITC Claimable: ₹2.07 lakh

Net Cost: ₹11.5 lakh (after ITC)

FAQ

Frequently Asked Questions

If your Bill of Entry has incorrect HS codes, mismatched invoice values, or inconsistent quantities compared to supporting documents, customs will usually raise queries, order extra examination, and may re‑assess duty, all of which delay clearance and increase costs.

As per amended Section 46, the BOE must generally be filed by the end of the day preceding the day of arrival of the vessel, aircraft or vehicle, and late filing can attract late fees and penalties from the customs department.

The BOE can be filed by the importer or by an authorised customs broker/CHA using their registered Customs House Agent code, typically via the ICEGATE portal using IEC‑linked login and DSC.

The filing process involves preparing documents, submitting data and documents electronically on ICEGATE, customs assessment by a customs officer, paying the applicable duties and IGST, and finally receiving Out of Charge for release of goods.

You must have a valid IEC, GST registration (if you want to claim ITC), ICEGATE registration, and a Class 3 DSC; many importers also formally appoint a CHA to manage the customs clearance process on their behalf.

Typical documents include the commercial invoice, packing list, Bill of Lading or Airway Bill, import licence (if applicable), insurance certificate, certificate of origin, and proof of duty/IGST payment, along with IEC, GSTIN and CHA authorisation letters.

The BOE is treated as the official record of each import transaction, used to support purchase accounting entries, IGST input tax credit claims, and later customs or GST audits and reconciliations.

Different BOE forms exist for home consumption, warehousing (Into‑Bond) and Ex‑Bond clearance from bonded warehouses, and special variants are used for re‑imports, transshipment and SEZ‑related movements.

This form is filed when imported goods are to be cleared into the domestic market immediately after paying all applicable customs duties and GST/IGST, and it is by far the most commonly used BOE type.

A BOE for warehousing allows goods to be moved into a customs‑bonded warehouse without immediate duty payment; duties and IGST are paid later when an Ex‑Bond BOE is filed to clear the goods for home consumption, helping importers manage cash flow.