Can You Claim Both 80C and 80D for Term Insurance? Know the Limits

Simplify Your International Payments

Skip the complexity of traditional wire transfers with EximPe's smart payment solutions

Complete international transfers in hours, not days, with real-time tracking

Streamline BOE and Shipping Bill regularization online, and generate e-BRCs effortlessly.

If saving taxes while guaranteeing your family’s future is important to you, understanding what insurance tax benefits are will be very helpful. Many people ask us at Eximpe: Can I use term insurance to claim both 80C and 80D deductions? It’s true—however, there are significant differences to consider. Below is a complete guide explaining how you can get the most from your term insurance tax benefits under the present Income Tax Act rules.

Understanding Term Insurance Tax Benefit Under Which Section

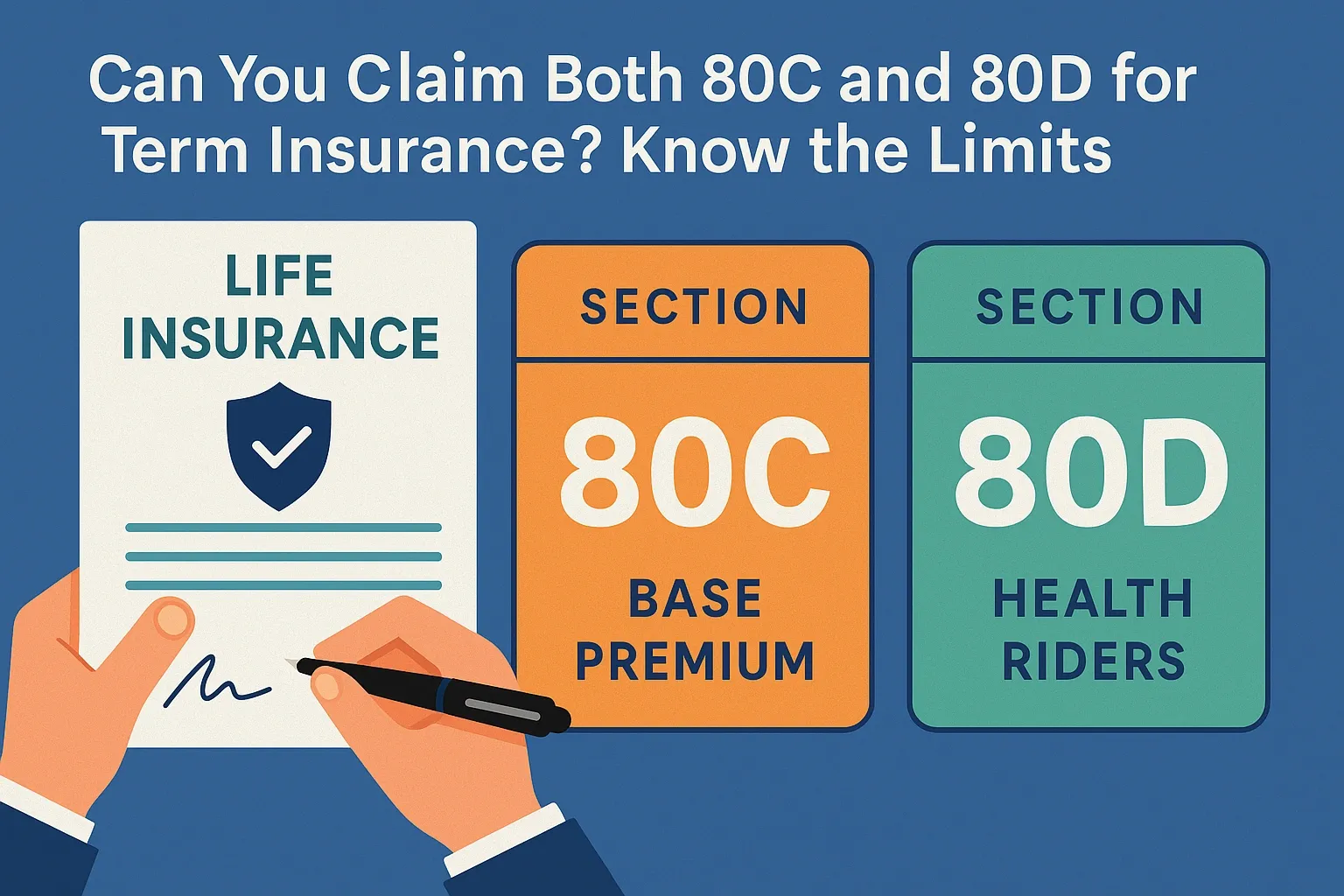

Term insurance offers tax benefits primarily under two sections of the Income Tax Act of 1961:

- Section 80C: For premiums paid towards the base term insurance policy.

- Section 80D: For premiums paid towards specific health-related riders (add-ons) attached to your term insurance, such as critical illness or hospital care riders.

Let’s break down how each deduction works and their respective limits.

80C Deduction for Term Insurance

What qualifies?

Expenses you pay for your term insurance policy are specifically covered by Section 80C.

Limit:

You can get benefits up to ₹1.5 lakh yearly, as all your eligible insurances, PPF, ELSS and NSC come under Section 80C.

- The annual premium for any policy issued after April 1, 2012, cannot be more than 10% of the sum assured to take advantage of the tax deduction.

- Should the policy be surrendered or ended during the first two years, the medical coverage deduction goes away.

Conditions:

80D Deduction for Term Insurance

What qualifies?

Most of what Section 80D is concerned with is health insurance premiums. If your term insurance allows a critical illness, hospital cash or surgical care rider, any premium you pay for these riders can be claimed under 80D.

- Get up to ₹25,000 a year for each of you, your spouse and children under 60 years.

- Additional insurance can be taken out for parents below 60 for ₹25,000 and ₹50,000 if parents are seniors.

- When you and your parents are both eligible, you can get a total deduction of ₹75,000 under 80D.

Important Note:

Limit:

Only health-related riders are entitled to a tax exemption, and the regular-term insurance premium does not qualify.

How to Maximize Term Insurance Tax Benefit

- You can claim tax exemption for the premium of your base term insurance.

- You can save tax by claiming a deduction of up to 80D for premiums you pay for eligible health riders with your term insurance.

- Properly organize your records and list what is needed on your taxes to gain the most out of these tax deductions.

Summary Table: Term Insurance Tax Benefits

Conclusion

If you know the difference between the base policy and these riders, you can claim both 80C and 80D deductions with your term insurance. The advantage of reducing your taxes and providing complete care for your family can be gained simultaneously. If you require personal tips on getting the most out of your term insurance tax benefit, contact EximPe today. Make sure you are covered in the future and pay less tax in the present—pick the right term insurance and use every advantage.

FAQs

- Can I claim both Section 80C and 80D deductions for my term insurance policy?

Yes, you can claim a deduction under Section 80C for the base term insurance premium and under Section 80D for premiums paid towards health-related riders like critical illness or hospital care attached to your term plan.

- What is the maximum deduction I can claim under Section 80C for term insurance?

You can claim up to ₹1.5 lakh per annum under Section 80C for premiums paid towards the base term insurance policy, subject to conditions on the mium-to-sum-assured ratio.

- Which term insurance premiums qualify for Section 80D deduction?

Only premiums paid for health-related riders (such as critical illness, hospital cash, or surgical care) attached to your term insurance qualify for Section 80D deduction—not the base premium itself.

- What are the Section 80D deduction limits for term insurance health riders?

You can claim up to ₹25,000 per year for yourself, spouse, and children (below 60 years), and up to ₹50,000 if covering senior citizen parents. The total can reach ₹75,000 if both you and your parents are eligible.

- What conditions must be met to claim these tax benefits?

For Section 80C, the annual premium should not exceed 10% of the sum assured for policies issued after April 1, 2012. For Section 80D, only health-related riders are eligible, and you must keep proper documentation for tax filing.

Simplify Your International Payments

Skip the complexity of traditional wire transfers with EximPe's smart payment solutions

Lightning Fast

Complete international transfers in hours, not days, with real-time tracking

Bank-Grade Security

Multi-layer encryption and compliance with international banking standards

Global Reach

Send payments to 180+ countries with competitive exchange rates