EDPMS & IDPMS: Complete Guide for Indian Importers and Exporters (2026 Update)

Complete IDPMS & EDPMS guide for Indian importers. Learn BOE-ORM matching, avoid caution listing, understand timelines, write-offs & compliances

Listen to article

Audio version (0% complete)

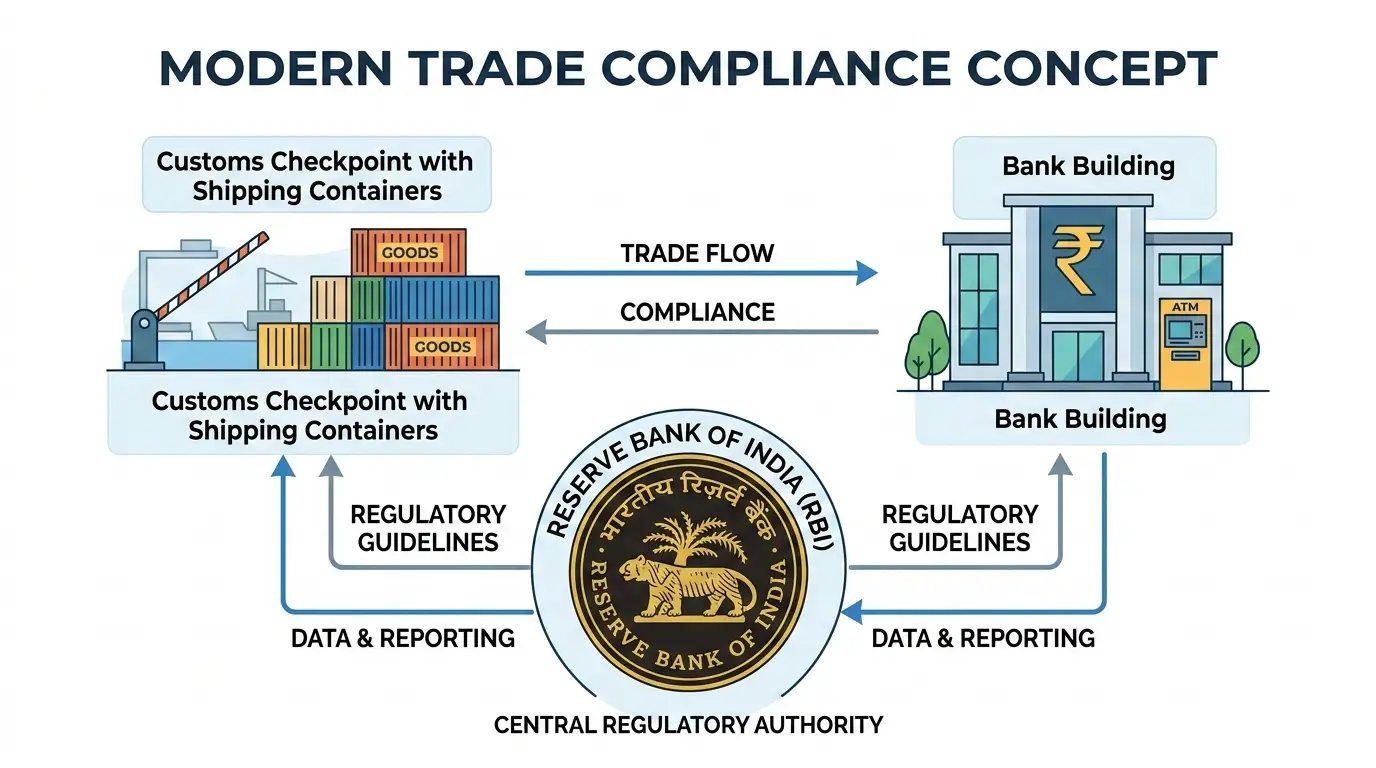

The Reserve Bank of India (RBI) runs two core trade-monitoring platforms: IDPMS for imports and EDPMS for exports. Together they connect Customs, authorised dealer (AD) banks, and RBI so that every dollar of foreign exchange going out or coming into India is matched with actual trade.

The Import Data Processing and Monitoring System (IDPMS) is RBI’s central digital platform to track import transactions from shipment to final payment. It went live nationwide on 10 October 2016 after pilot work and system changes at banks and Customs.IDPMS links Customs’ Bill of Entry (BoE) data with your AD bank’s outward remittance data so that every payment in foreign currency is backed by genuine goods entering India. On the other hand, EDPMS tracks shipping bills and realisation of export proceeds, replacing the old physical FIRC regime with electronic eBRCs.

Why IDPMS Exists

RBI’s working group recommended a robust IT system to replace fragmented, paper‑based import monitoring and to tighten control over foreign exchange outflows. The stated objective is to “facilitate efficient processing of all import transactions and effective monitoring thereof,” ensuring payments align with actual BoEs filed at Customs.In practical terms, IDPMS helps prevent:

- Over‑invoicing or fake imports to siphon money out of India.

- Long‑pending, unreconciled import payments that never get matched with BoEs.

- Gaps in FEMA reporting across different banks and ports.

How IDPMS Integrates the Ecosystem

IDPMS works on a three‑way data flow:

- Customs / ICEGATE: Generates and uploads BoE data (BoE number, date, port, value, importer IEC, AD code) to RBI’s secure server.

- RBI IDPMS server: Acts as the central hub, distributing BoE data to the relevant AD bank based on the AD code.

- AD banks: Download BoEs daily, capture outward remittance data (ORM), and match BoE–ORM pairs to close import transactions. This integration ensures that every rupee of foreign currency sent abroad via the banking system is traceable back to a specific BoE and importer under FEMA.

2. What Is EDPMS?

The Export Data Processing and Monitoring System (EDPMS) is RBI’s platform for tracking export shipments and the realisation of export proceeds. EDPMS has been operational since March 2014 and centralises export reporting that was earlier scattered across multiple returns and statements. Its core objective is to ensure exporters actually receive and repatriate foreign currency for goods or services shipped abroad within prescribed timelines. That realisation is what finally lets a shipping bill be closed, here's the full walkthrough of shipping bill closure in EDPMS.

From Physical FIRC to eBRC

Before EDPMS, banks issued a physical Foreign Inward Remittance Certificate (FIRC) for each export‑related remittance. In May 2016 RBI decided to discontinue issuing physical FIRCs for export payments and instead route all such data through EDPMS. Since June 20, 2016, banks issue electronic FIRCs (e‑FIRCs) and then generate electronic Bank Realisation Certificates (eBRCs) from EDPMS data. Today, eBRCs pulled from EDPMS are mandatory for GST refunds and export incentive claims with DGFT and tax authorities.

Why This Matters to Exporters

For exporters, EDPMS does the mirror job of IDPMS:

- Captures shipping bill data from Customs and other export platforms (SEZ, STPI).

- Monitors whether export proceeds are realised within the allowed period.

- Automates caution listing/de‑caution listing of exporters with long‑pending shipping bills.

How IDPMS Works: 10‑Step Import Lifecycle

The IDPMS lifecycle for a typical goods import can be broken into ten practical steps.

- Import Shipment Initiated

The importer places a purchase order and the overseas supplier ships goods toward India under agreed Incoterms.

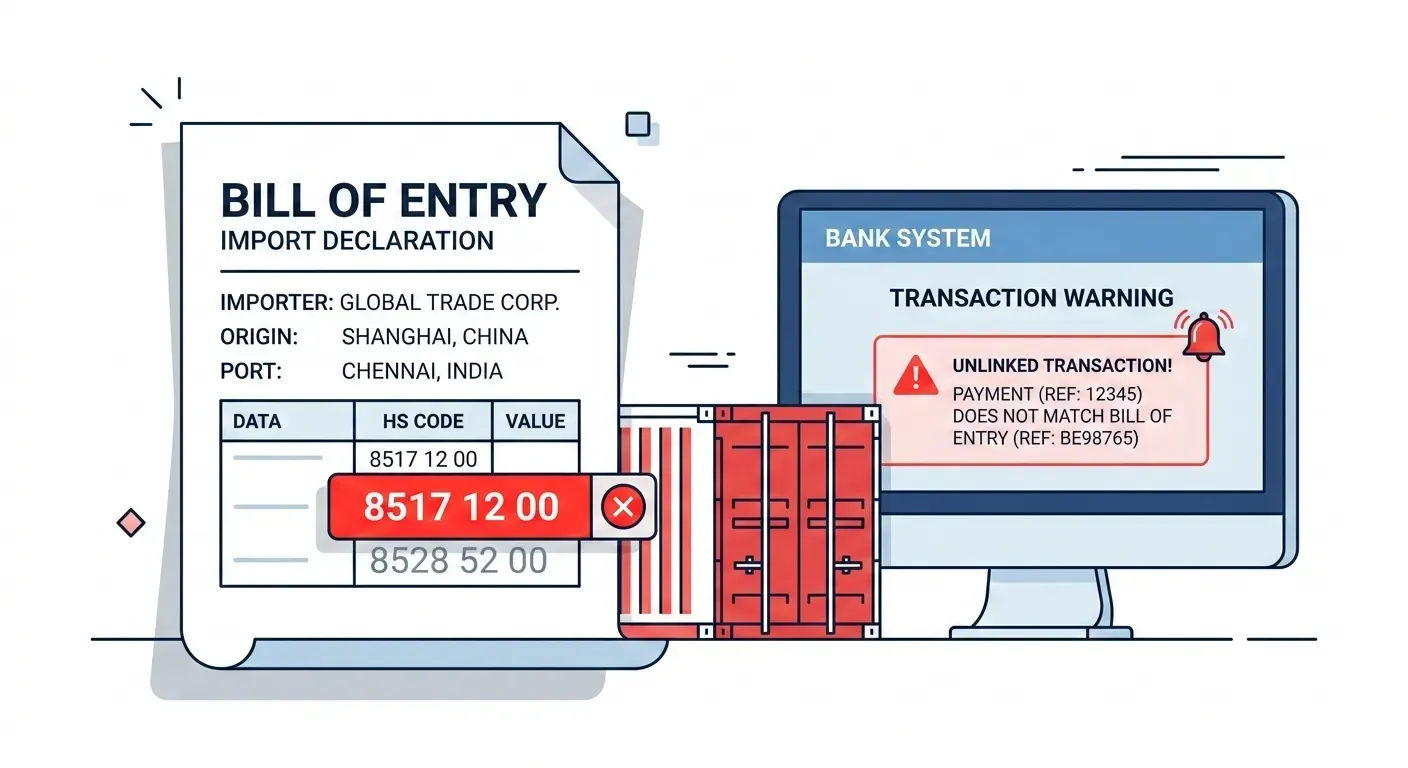

- Bill of Entry Filed at Customs

On arrival, the Customs House Agent (CHA) files the BoE at the port or airport via ICEGATE, with correct IEC details and a valid 14‑digit AD code of the importer’s bank.

- BoE Data Transmitted to RBI

For EDI ports, Customs automatically pushes BoE data to RBI’s IDPMS server, for non‑EDI/manual ports, the importer’s AD bank uploads BoE details using the “Manual BoE Reporting” message.

- BoE Appears in Bank’s IDPMS Queue

The BoE now shows as an “outstanding import bill” or open BoE in the AD bank’s IDPMS dashboard, waiting to be linked to payment.

- Document Submission to Bank

The importer submits BoE, commercial invoice, packing list, transport document (BL/AWB), and any other required papers to the AD bank. The bank uses these to verify that the BoE genuinely belongs to the importer and to map it correctly in IDPMS.

- Import Payment Processed

The importer remits payment (advance or post‑shipment) through the AD bank via SWIFT/wire transfer, letter of credit negotiation, or other permitted modes under the Master Direction. The bank processes the remittance subject to KYC and FEMA checks.

- ORM (Outward Remittance Message) Generated

For each eligible outward remittance, the AD bank creates an Outward Remittance Message (ORM) in IDPMS as mandated by RBI. The ORM is a unique digital acknowledgement of the payment.

- Payment Matching in IDPMS

The bank matches ORM entries with corresponding BoEs using the “BoE Settlement” message format. Multiple ORMs can settle a single BoE and, conversely, a single large ORM can be apportioned against multiple BoEs.

- BoE Closure

Once the bank is satisfied that payments and documents align with the BoE value (after permissible write‑offs or adjustments), it marks the BoE as “closed” in IDPMS.

- Overdue Monitoring & Escalation

If BoEs remain unmatched or partially settled beyond permitted timelines, they appear as overdue or outstanding entries. Banks must follow up with the importer, may report cases for caution listing, and in serious situations regulators can initiate enforcement or compounding.

A simple example: A manufacturer imports raw material worth ₹50 lakh on 90‑day credit and pays in three instalments. The bank will see one BoE for ₹50 lakh, three ORMs over 90 days, and then close that BoE once all three ORMs are mapped and minor differences (FX, charges) are adjusted.

AD Code (Authorised Dealer Code)

An AD code is a 14‑digit identifier issued by your AD bank that links your current account and branch to Customs and RBI systems. You must register this code on ICEGATE for each port where you file shipping bills or BoEs, without it, Customs systems cannot route BoE data to the correct bank.

A wrong or missing AD code means your BoE may not land in your bank’s IDPMS queue at all, making payment reconciliation almost impossible until the BoE is amended or the code corrected.

How to Check IDPMS Status Online

Importers cannot log in to IDPMS directly, but there are two practical ways to track BoE status.

Option 1: ICEGATE “Status of BE in RBI‑IDPMS”

The ICEGATE portal provides a public service called “Status of BE in RBI‑IDPMS” which lets you check whether a specific BoE has been transmitted to and processed in IDPMS. You typically need:

- BoE number.

- BoE date.

Location/port code.The portal then displays BoE details and the date of transmission to RBI/IDPMS, helping you confirm that Customs data has reached your bank’s system.

Option 2: Through Your AD Bank

AD banks have full dashboard access to IDPMS and can generate reports of all outstanding, matched, and closed BoEs for each importer. Many banks now share monthly IDPMS statements or on‑demand snapshots, which are valuable for early detection of mismatches or overdue entries.

Common IDPMS Mistakes That Hurt Importers

Practical experience shows most IDPMS issues are preventable and arise from process gaps rather than fraud.

- Delayed BoE submission to bank: When importers do not share BoE copies promptly, banks cannot verify or link entries. Persistent delays may lead to repeated reminders, service charges, and eventually caution‑listing recommendations.

- Invoice–payment mismatch: FX fluctuations, bank charges, discounts, or freight/insurance adjustments can cause ORM amounts to differ from BoE values. If importers do not proactively explain these differences, BoEs remain open.

- Wrong or missing AD code on BoE: An incorrect AD code at the time of BoE filing routes the BoE to the wrong bank or leaves it unlinked, correction later can be time‑consuming. Until fixed, your own bank’s IDPMS will show outstanding ORMs without corresponding BoEs.

- Non‑updated shipping details or returns: If part shipments, returns, or short shipments are not communicated to the bank with supporting documents, BoE values appear inconsistent with payments.

- Ignoring overdue entries: Leaving overdue BoEs unattended is risky; banks are required to escalate such cases, which can trigger caution listing, FEMA scrutiny, and in high‑value matters, attention from enforcement agencies.

IDPMS vs EDPMS: At‑a‑Glance

Aspect | IDPMS (Imports) | EDPMS (Exports) |

Direction of funds | Forex outflow from India | Forex inflow into India |

Primary purpose | Track import payments and ensure they match BoEs | Track export shipments and ensure proceeds are realised |

Core customs document | Bill of Entry (BoE) | Shipping Bill |

Bank document link | ORM matched with BoE for closure | Inward remittance matched with Shipping Bill and reflected in eBRC |

Main risk of non‑compliance | Caution listing, FEMA penalties, possible ED scrutiny | Caution listing, denial of incentives, FEMA penalties |

User access | No direct importer login; accessed via AD banks and ICEGATE BoE status | No direct exporter login; status via AD banks and DGFT/eBRC systems |

FEMA 2025–26: What’s Changing for Trade

RBI is overhauling its export‑import regulations under FEMA through a combination of formal amendments and draft regulations expected to become fully effective in the coming years.

Small-Value Self-Declaration Closure (₹10 Lakh Rule)

In October 2025, RBI issued A.P. (DIR Series) Circular No. 12 / 2025‑26 to permanently simplify the closure of small-value entries in both EDPMS and IDPMS. This is a major relief for MSME/ E-commerce exporters and importers who frequently deal with low-ticket invoices.

Key points you should know:

- Threshold: AD Category-I banks can now reconcile and close export and import entries of value up to ₹10 lakh per shipping bill/Bill of Entry (per entry/bill) based only on a declaration from the exporter or importer.

- What you declare:

- Exporter declares that export proceeds have been realised.

- Importer declares that payment for imports has been made.

- No detailed scrutiny for small tickets: For these small entries, banks are not required to insist on full document trails or extensive discrepancy explanations. The self-declaration is sufficient, subject to basic sanity checks.

- Invoice value reductions allowed: If the final realised/paid amount is lower than the original invoice/shipping bill/Bill of Entry value (for example due to discounts, quality claims, or short shipment), banks can accept the reduced value purely on the basis of the same declaration.

- Quarterly consolidated statements: To handle volume efficiently, exporters and importers can submit one consolidated declaration per quarter covering multiple small-value entries instead of dealing with each bill separately.

- No penal charges for delay: RBI has directed banks to avoid penal charges for regulatory delays in these small-value EDPMS/IDPMS closures and to rationalise service charges so that fees remain reasonable relative to transaction size.

- Applies to outstanding entries too: The facility is available not only for fresh bills but also for legacy pending entries under ₹10 lakh that are clogging up EDPMS/IDPMS, subject to the same declaration process.

In simple terms: if your per-bill value is ₹10 lakh or less, you can now work with your bank to close those entries faster with far less paperwork—just a properly worded declaration that payment has been received or made. This is one of the most practical ease-of-doing-business changes for small importers and exporters in recent years.

FAQs

Frequently Asked Questions

If documents and payments line up cleanly, banks can usually close an IDPMS entry within about a week of receiving complete information, though complex cases take longer.

BoEs that remain unmatched beyond allowed periods are flagged as overdue, banks must follow up, may restrict trade facilities, and can recommend caution listing.

Existing and draft regulations allow routing payments via different ADs as long as transactions are reported correctly, in practice, banks coordinate through ORMs and BoE data sharing when importers inform them in advance.

Minor discounts or value reductions can usually be handled via write‑off provisions (5% rule) or, for small‑value bills, via the ₹10 lakh declaration route, larger reductions require more robust documentation.